Business Growth @ ABC

[Submittted by Indranil Sen Gupta,

Financial, Economic Writer and Research Analyst,

Kolkata, West Bengal]

August 04, 2010

We often find that any business begins with a speedy opening session and later on slows down in business generation. The management drill very deep to find the reason and finally the conclusion come out that the plan or the people engaged in business failed. Frankly speaking they get ready with the drill process but never drill deep to find the correct reasons for the failure. May be they suppressed their own facts of wrong decision making.

I remember and you too can that we find a broking company runs with this theory that if we start on with a theory like shop at each corner then business will grow and competitors will the thrown out of the box. The concept is wrong. Look out for all those entrepreneurs .They started their business with one shop and later on came with 100.They did not start with 100 and later on came to 10.The reason is not lack of funding etc. The reason is that one needs to grow slowly and then reach out at one time with climbing high towards the top of the mountain.

You might start up with 100 and when you fail at any point of time you have to wind up the decision once taken by you. Forget about the capital loss and manpower loss happened due to closures. Forget about break even and other calculations. Just explain how you will make up the lost goodwill in the hands of the clients you started off. You jeopardized the system and the goodwill and made the game more tough for the rest of the existing people in the system. We find this type of examples in retail business, pharma, broking, financial products market in fact in every corner.

Development does not mean that you need to start a business with 100 outlets. Development has this meaning also that from one corner office you expand it to total 10 floor office. Decision makers often fail here. What we need is not solution. We need problems and the question what next.

Another factor we need to keep in mind is that you cannot play the same game at every corner. It means that when you open a shop you need to have a clear idea of your buyers. Now many of us will say that we know our buyers. Drill again here. Very deep we find that knowing preference and tastes of customers is a different ball game but are the numbers of customers are increasing. Now one might say that why we have sales team here. Great .But can they breed customers.

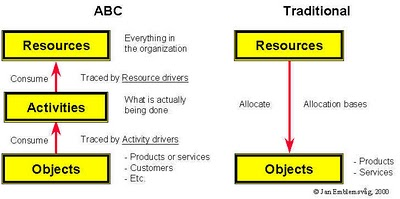

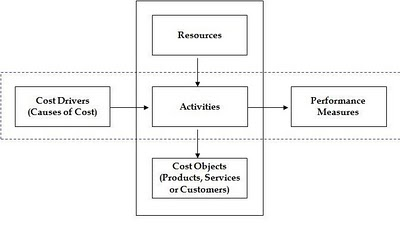

It now might sound funny. Let me give you all an example. Say you have a box of 10 apples. You consume 8 apples in 8 days. You are now left with 2 apples. You go out into the market and you get another 10 apples and finally you have 12 apples. Now imagine you went to the market and found no apple and only oranges what will you do. The problem is this that you need to identify the pool of resources being generated. That will help you to identify the place of opening your shop. This is called resource allocation according activity. The below image will make it more clear itself.

For example in Kolkata you have management institutes. Students pass out and gets placements. That is very good news since they will now start earning and consumption will pick up and more growth in sales. But all placements are outside of Kolkata. Now the pool of income is happening in other places but you opened your outlet say 50 in Kolkata alone and kept another 50 outlets spread across India. Is the process is related to activity based. What you need is activity based costing.

Pooling the resources according to the measured activity and finally achieving the growth. Activity-based costing (ABC) is a costing model that identifies activities in an organization and assigns the cost of each activity resource to all products and services according to the actual consumption by each: it assigns more indirect costs (overhead) into direct costs.

In this way an organization can precisely estimate the cost of its individual products and services for the purposes of identifying and eliminating those which are unprofitable and lowering the prices of those which are overpriced.

In a business organization, the ABC methodology assigns an organization's resource costs through activities to the products and services provided to its customers. It is generally used as a tool for understanding product and customer cost and profitability. As such, ABC has predominantly been used to support strategic decisions such as pricing, outsourcing, identification and measurement of process improvement initiatives.